The Forward Transition Shadow as a Negotiation Corridor

- January 5, 2026

- Posted by: DrGlenBrown2

- Category: Quantitative Trading Systems

Forward Transition Shadow Series — Part 3

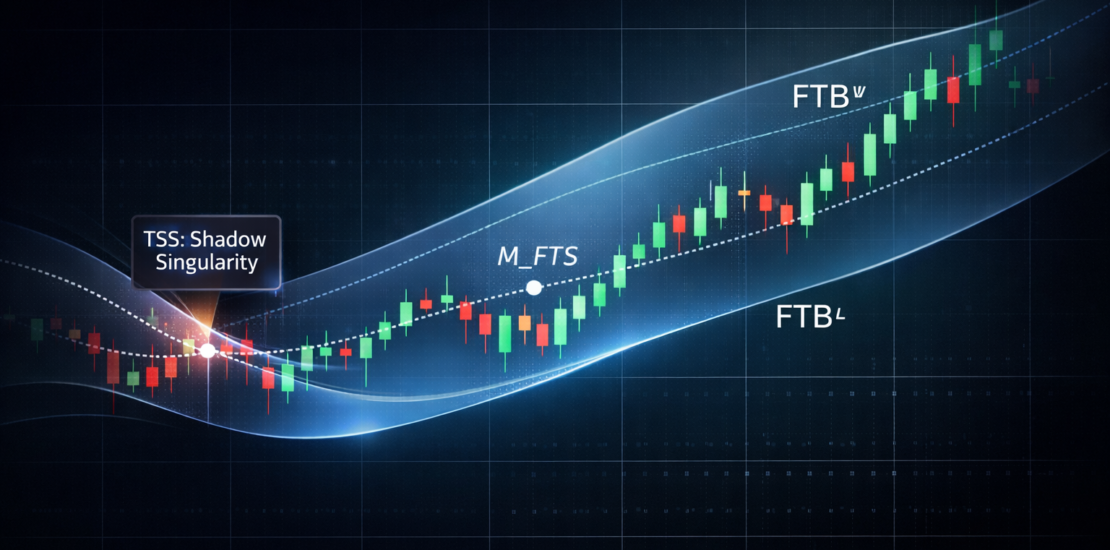

This article expands on the Forward Transition Boundary (FTBᵁ / FTBᴸ) and Forward Transition Shadow (FTS) doctrine within the GATS Framework. The full and authoritative doctrine is published here: Forward Transition Boundary (FTB) & Forward Transition Shadow (FTS) .

1. From Boundary to Corridor

Traditional EMA analysis treats structure as a set of lines. The Forward Transition Shadow reframes structure as a corridor.

Rather than asking whether price is simply above or below a single reference, the FTS evaluates how price behaves relative to a band of forward-staged structural memory.

This subtle shift changes interpretation entirely. The question is no longer:

“Did price cross the line?”

It becomes:

“How is price negotiating with remembered structure?”

2. The Three Structural States of the Shadow

2.1 Price Above the Shadow — Structural Dominance

When price closes decisively above FTBᵁ, it is operating above the forward-projected memory of the Transition Zone.

This condition reflects:

- Acceptance of higher prices

- Coherent trend continuation

- Minimal need for renegotiation

In this state, the shadow acts as a trailing structural reference, not an obstacle. Pullbacks tend to be shallow and brief.

2.2 Price Inside the Shadow — Negotiation

When price trades within the Forward Transition Shadow, the market is actively reconciling current price with prior structural agreement.

This is not noise. It is structured negotiation.

Inside the corridor, the market decides whether:

- The existing trend will resume

- The structure will compress into range

- The regime will destabilize

For GATS users, this zone demands discipline. Entries require confirmation and patience. Impulsive participation here is a common source of drawdown.

2.3 Price Below the Shadow — Structural Invalidation

When price closes below FTBᴸ, it has violated the remembered Transition structure.

This condition implies:

- Loss of structural continuity

- Elevated probability of regime change

- Increased risk for trend-aligned positions

Importantly, this is not a mandatory reversal signal. It is a posture shift—from participation to caution or non-participation.

3. Why the Shadow Is a Corridor, Not Support or Resistance

It is tempting to treat the Forward Transition Shadow as a dynamic support or resistance zone. This interpretation is incomplete.

Support and resistance describe reaction levels. The FTS describes structural legitimacy.

Price may move freely inside the corridor without producing tradeable signals. What matters is whether the market ultimately:

- Reclaims dominance

- Remains trapped in negotiation

- Invalidates structure

4. Pullbacks Reclassified by the Shadow

The Forward Transition Shadow allows pullbacks to be classified precisely:

- Type I Pullback: Price retraces toward the shadow but holds above FTBᵁ (trend intact).

- Type II Pullback: Price enters the shadow and stabilizes (controlled negotiation).

- Type III Pullback: Price exits below FTBᴸ (structural warning).

This classification replaces vague notions of “healthy” vs “unhealthy” pullbacks with a repeatable structural framework.

5. Discipline Inside the Corridor

The negotiation corridor is where overtrading occurs. The FTS exists, in part, to prevent this.

Inside the shadow:

- Risk should be sized conservatively

- Confirmation thresholds should be higher

- Non-participation is often the correct decision

This reinforces a core GATS principle:

Capital preservation is a decision, not a by-product.

6. Relationship to the Master Doctrine

This article explains how to interpret the Forward Transition Shadow as a negotiation corridor. It does not alter definitions, parameters, or rules.

All formal specifications—including the Forward Transition Boundaries, shadow width, midline equilibrium, and Transition Shadow Singularity (TSS)— are defined exclusively in the master doctrine:

Forward Transition Boundary (FTB) & Forward Transition Shadow (FTS) .

Next in the series:

Forward Transition Shadow Series — Part 4: Shadow Width, Compression, and Structural Stress

About the Author

Dr. Glen Brown is President & CEO of Global Accountancy Institute, Inc. and Global Financial Engineering, Inc., proprietary trading firms specializing in institutional trading systems, volatility-aware risk management, and multi-timeframe market structure design through the GATS Framework.

Business Model Clarification

Global Accountancy Institute, Inc. and Global Financial Engineering, Inc. operate exclusively as proprietary trading firms. All concepts discussed are provided for educational and informational purposes only and do not constitute investment advice or an offer to manage external capital.

General Disclaimer

This content is for educational purposes only and does not constitute financial, legal, or investment advice. Trading decisions are the sole responsibility of the reader. Examples are illustrative and not indicative of future performance.

Risk Disclaimer

Trading financial markets involves substantial risk and may result in the loss of some or all invested capital. Past performance is not indicative of future results. Always assess your risk tolerance and seek independent professional advice where appropriate.