-

Lecture 7: The Law of Drawdown in Time — Quantum Implications for Trade Longevity

- November 2, 2025

- Posted by: DrGlenBrown2

- Categories: GATS Lecture Series — Algorithmic Risk and Volatility Engineering, GATS Methodology

No Comments

This lecture formalizes the GATS axiom that drawdown should cost time, not capital. We map equity drawdown to a temporal budget via ATR-regime geometry and codify how DS (Death-Stop), DAATS (Dynamic Adaptive ATR Trailing Stop), and the 18.75% Law synchronize to convert equity risk into structured time expenditure. We then extend this to portfolio heat, shock handling, and “Exit Only on Death” discipline, with quantitative tables and MT5/GATS implementation blocks.

-

Lecture 6: The Geometry of Time — Trade Lifecycles, Resonant Durations, and Temporal Compression within GATS

- November 2, 2025

- Posted by: DrGlenBrown2

- Categories: GATS Lecture Series — Algorithmic Risk and Volatility Engineering, GATS Methodology

This lecture develops the Temporal Geometry Model within the Global Algorithmic Trading Software (GATS). Each trade is treated as a temporal organism whose lifespan expands or contracts with volatility, multi-timeframe alignment, and the 18.75% adaptive law. We formalize Temporal Compression (TC), Resonant Duration (Tres), and Chrono-Risk Scaling, and provide MT5/GATS execution patterns that convert volatility into measurable time.

-

Lecture 4: The 18.75% Law of Adaptive Transition — Symmetry Between Breakeven and Trail

- November 2, 2025

- Posted by: DrGlenBrown2

- Categories: GATS Lecture Series — Algorithmic Risk and Volatility Engineering, GATS Methodology

This lecture formalizes the 18.75% Law of Adaptive Transition within the Global Algorithmic Trading Software (GATS). The law defines the universal threshold at which a trade shifts from survival to expansion: the breakeven activation and the ongoing trail amplitude are both set to 3/16 of the Death-Stop (DS). By unifying these thresholds, GATS encodes a structural symmetry that converts drawdown into time and momentum into measured respiration. We provide derivations, tables, and MT5/GATS implementation logic for multi-asset deployment.

-

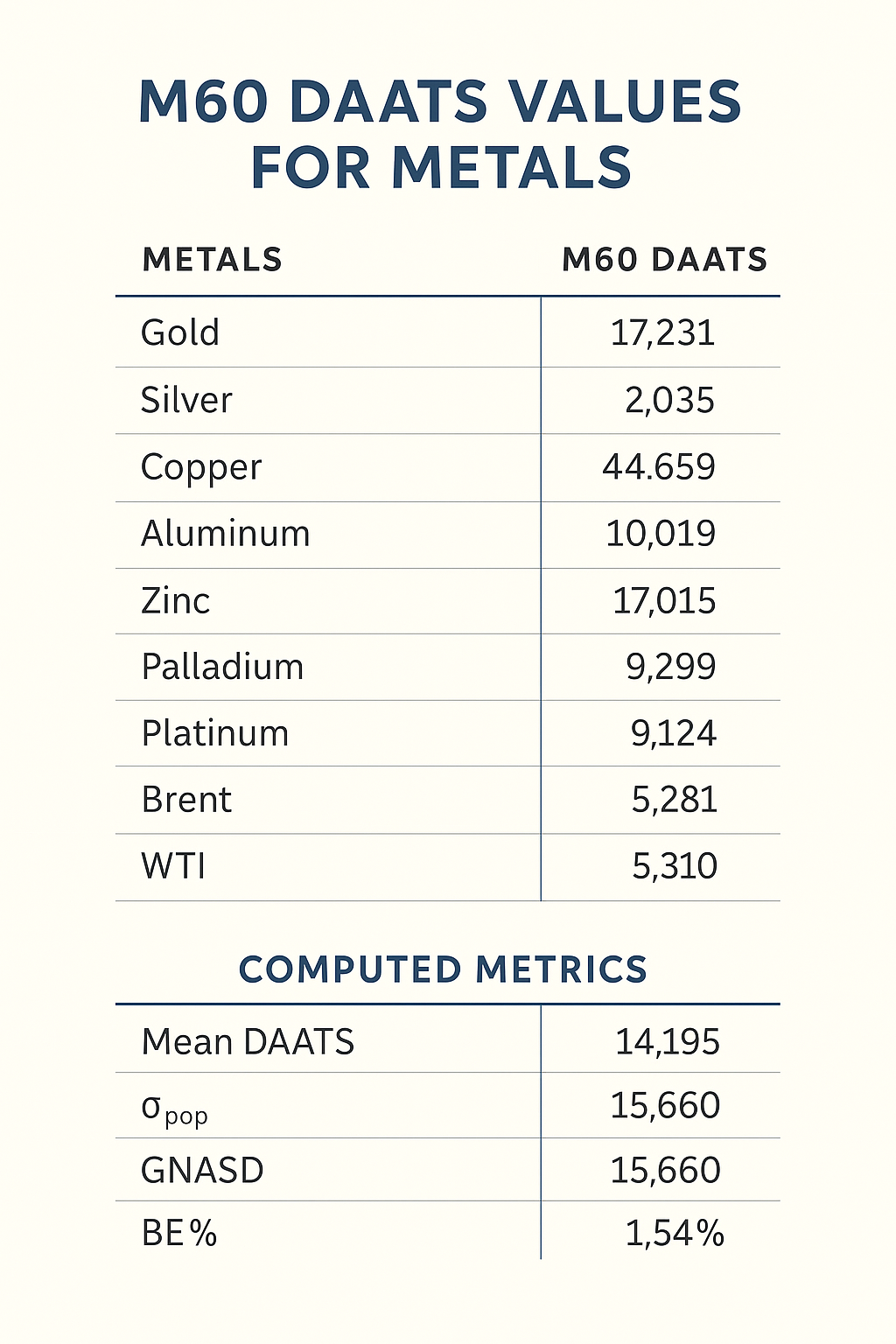

Calculating GNASD & BE% for an M60 Metals Portfolio

- June 2, 2025

- Posted by: DrGlenBrown2

- Category: GATS Methodology

Learn how to compute portfolio σpop, GNASD (one-sigma noise unit), and BE% for 10 metals (Gold, Silver, Copper, Aluminum, Zinc, Lead, Palladium, Platinum, Brent, WTI) using updated M60 DAATS values.

-

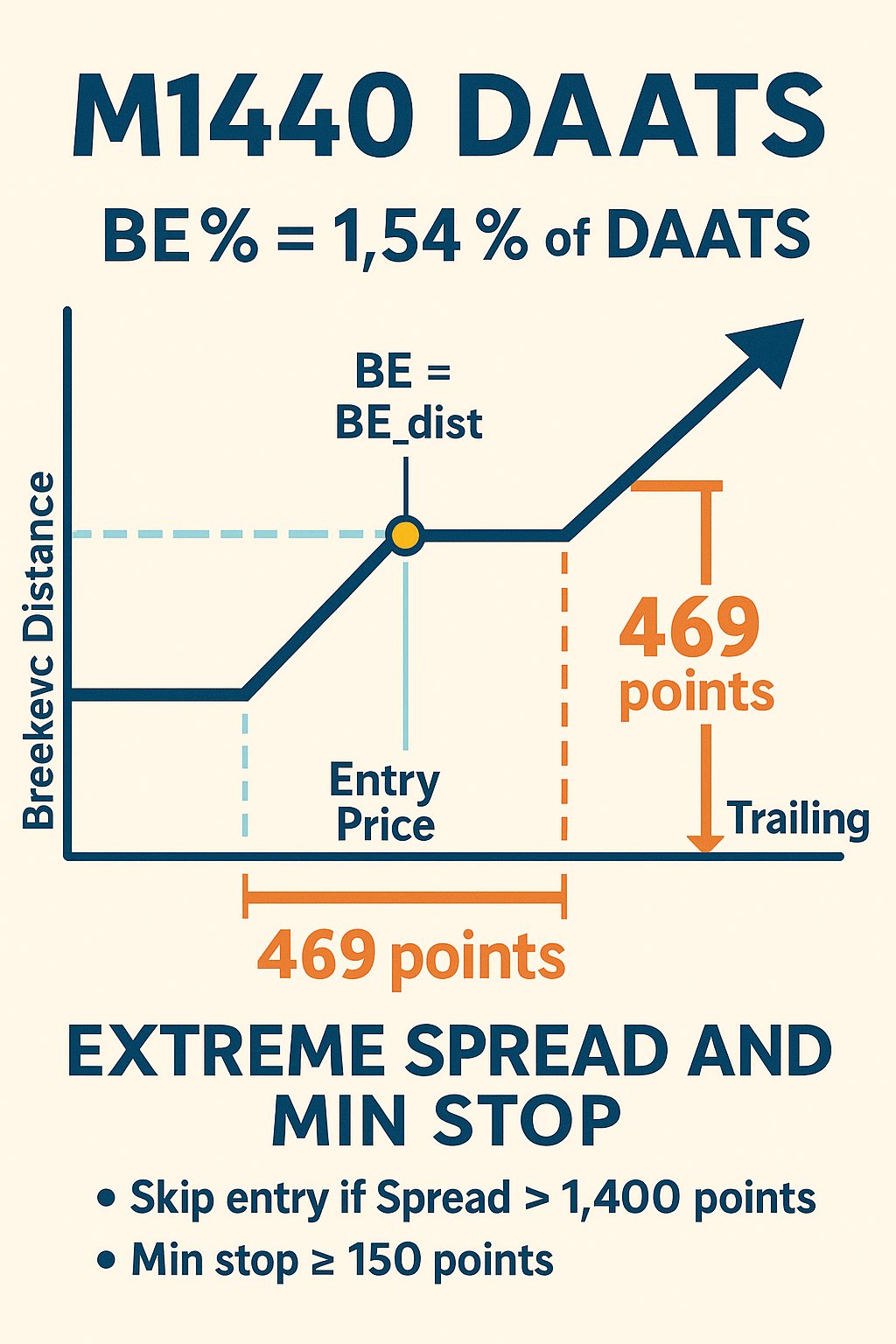

Final M1440 DAATS Lecture: Breakeven & Trailing Stops with Extreme Spread Handling

- June 1, 2025

- Posted by: DrGlenBrown2

- Category: GATS Methodology

Learn our final M1440 DAATS framework for 28 forex pairs: BE % = 1.54 % of DAATS, post‐BE trailing = 469 points, and skip entries if spread > 1 400 points, all aligned with Dr. Brown’s Seven Laws.

-

Applying M60 DAATS & GNASD Logic to Equities: GEMF – USA Sub‐Fund

- May 31, 2025

- Posted by: DrGlenBrown2

- Category: GATS Methodology

Learn how GEMF – USA Sub-Fund uses M60 DAATS and GNASD to set stop floors, breakeven triggers, and trailing stops on micro-timeframes (M30, M15, M5, M1) under the Daily MACD bias and M60 EMA regime.

-

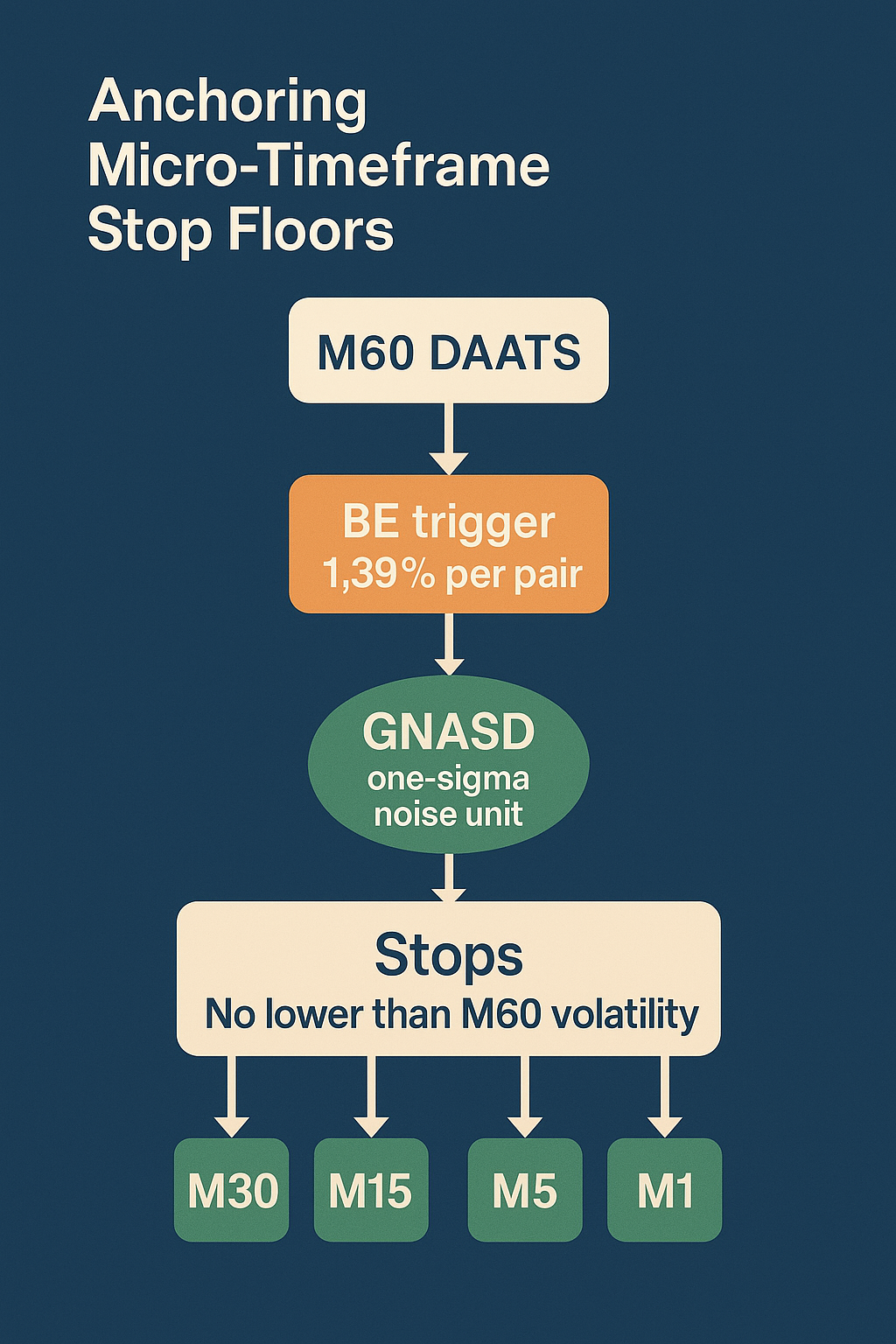

Micro‐Timeframe Stop Floors & Breakeven Logic Using M60 DAATS & GNASD

- May 31, 2025

- Posted by: DrGlenBrown2

- Category: GATS Methodology

In this lecture, we demonstrate how GATS leverages M60 DAATS and the portfolio’s one‐sigma noise unit (GNASD) to establish robust stop‐loss floors, breakeven triggers, and trailing stops on M30, M15, M5, and M1. By anchoring micro‐timeframe stops to hourly volatility and applying a 1.39% breakeven rule per pair, traders can avoid routine hourly whipsaw while still capturing high‐probability moves under the Daily MACD bias and M60 EMA regime filters.

- 66 W Flagler Street, Suite 900-8535, Miami, FL 33130

- info@globalaccountancyinstitute.com

- +1 786-305-3315