Market Expected Moves Hypothesis (MEMH): Forecasting the Next Swing

- May 6, 2025

- Posted by: DrGlenBrown2

- Categories: Blog, Quantitative Finance / Risk Management

Objective: Present MEMH theory, statistical underpinnings, and its overlay on target-setting.

Audience: Quant researchers, portfolio managers.

Outline:

- MEMH concept & academic roots

- Calculating expected moves per timeframe

- Setting profit targets & stop levels

- Case studies in equities & FX

Executive Summary

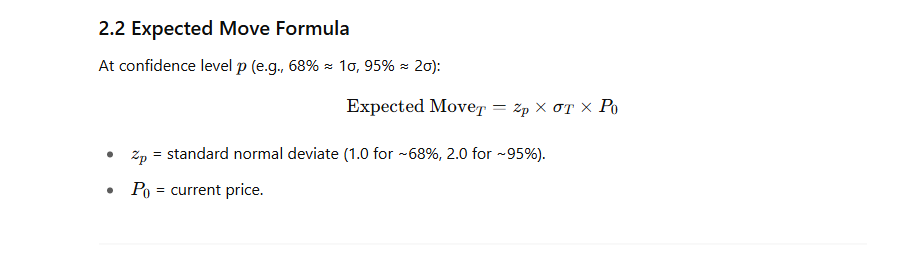

Dr. Glen Brown’s Market Expected Moves Hypothesis (MEMH) equips traders with a statistically grounded method to anticipate price‐swing magnitudes by harnessing volatility‐adaptive stops (DAATS). At its core is the Market Daily Average Expected Move (MDAEM) formula:

where DAATSM1440_{\text{M1440}}M1440 uses a 200-period Average True Range (ATR) across all timeframes. By standardizing on ATR-200 and empirically calibrating the 0.6375 factor, MEMH offers clear profit‐target and stop‐placement rules adaptable to any timeframe or asset class.

1. MEMH Foundations & DAATS Integration

Dynamic Adaptive ATR Trailing Stops (DAATS) adjust exit levels to current volatility. Under MEMH, we:

- 4-Hour (M240):

ATR200,4H measures 4-hour volatility. - Hourly (M60), 30-Minute (M30), etc.:

Same ATR-200 base, scaled by 15, then multiplied by 0.6375.

This ensures consistency: an “expected move” on M240 and M1440 share the same volatility foundation and statistical factor.

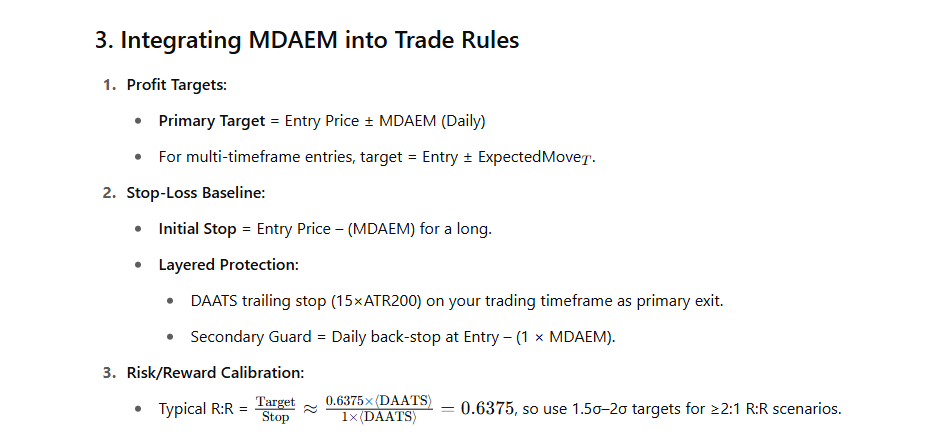

3. Integrating MDAEM into Trade Rules

4. Case Studies

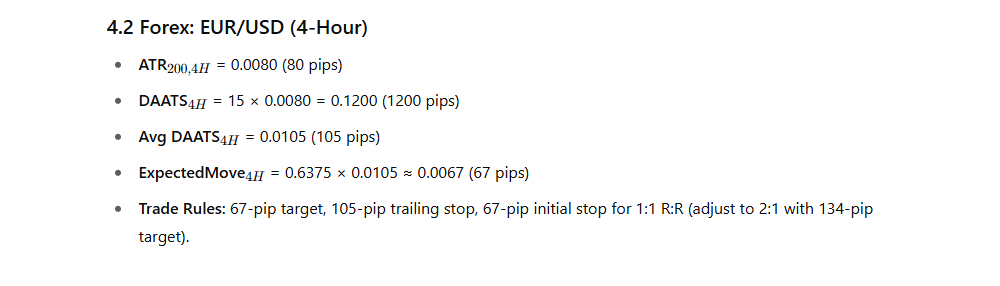

4.2 Forex: EUR/USD (4-Hour)

5. Conclusion

By anchoring expected‐move forecasts to average DAATS—all measured on a standardized ATR-200 base—and applying the 0.6375 factor, MEMH delivers a transparent, cross-asset, cross-timeframe framework for setting realistic profit targets and informed stop placements. This unification with GATS’s volatility‐adaptive architecture ensures every strategy benefits from consistent, statistically-driven guidance.

About the Author

Dr. Glen Brown, President & CEO of Global Accountancy Institute, Inc. and Global Financial Engineering, Inc., holds a Ph.D. in Investments and Finance. He pioneered MEMH to harmonize volatility‐adaptive stops with statistical price‐move forecasting, empowering traders with clear, data-driven decision rules.

Risk Disclaimer

This article is for educational purposes and does not constitute investment advice. MEMH relies on historical ATR-200 volatility and normal-distribution assumptions, which may fail in extreme regimes. Always backtest thoroughly and consult qualified professionals before live deployment.