-

The October 2025 Peak Reclassified: The First ETF Mass Saturation Event

- January 4, 2026

- Posted by: DrGlenBrown2

- Category: Market Structure & Risk Doctrine

No Comments

Why the October 2025 Bitcoin peak marks Bitcoin’s institutional rebirth under ETF gravity.

-

The EGAML State Machine: Why Bitcoin Must Be Classified A/B/C Before Trading

- January 3, 2026

- Posted by: DrGlenBrown2

- Category: Market Structure & Risk Doctrine

A doctrine-grade explanation of the EGAML State Machine—why Bitcoin must be classified into State A, B, or C before any trading decision in the ETF era.

-

ETF Gravity Wells: How Creation/Redemption Alters Price Behavior

- January 3, 2026

- Posted by: DrGlenBrown2

- Category: Market Structure & Risk Doctrine

A doctrine-grade explanation of ETF “gravity wells”—how creation/redemption translates capital flows into absorption, extension, or vacuum regimes in Bitcoin under EGAML.

-

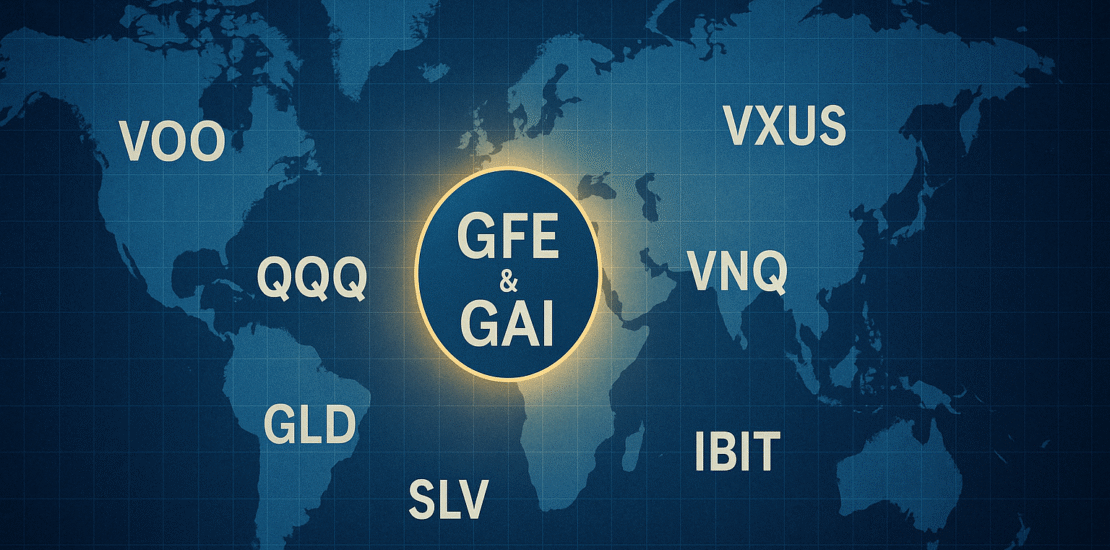

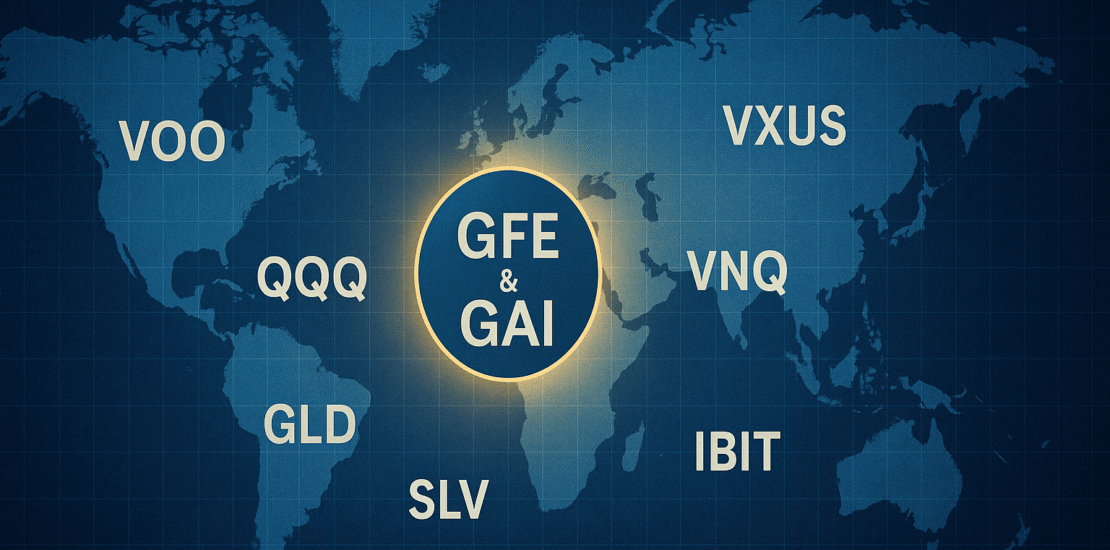

Global Multi-Asset ETF Portfolio White Paper v1.0 – GAI & GFE

- November 28, 2025

- Posted by: DrGlenBrown2

- Categories: Global Proprietary Trading Research, Research & White Papers

This white paper presents the Global Multi-Asset 50-ETF Portfolio engineered for Global Accountancy Institute, Inc. and Global Financial Engineering, Inc. It unifies GATS, the Universal Risk Doctrine (DS = 16 × ATR256), the 1–9% timeframe-indexed risk model, and the Nine-Laws Framework into a single proprietary trading doctrine for cross-asset, multi-timeframe execution.

-

Global Multi-Asset ETF Master Portfolio for GFE & GAI

- November 28, 2025

- Posted by: DrGlenBrown2

- Category: Global Multi-Asset Portfolios

Discover the Global Multi-Asset ETF Master Portfolio designed by Dr. Glen Brown for GFE & GAI, integrating GATS, DAATS, and the Nine-Laws Framework into a unified, institution-grade ETF universe.

-

Guidex Theory – Reframing Digital Currencies as a Global Kinetic Energy Matrix

- November 25, 2025

- Posted by: DrGlenBrown2

- Categories: Digital Asset Research, Quantitative Research, Research & White Papers

Guidex Theory – White Paper v1.0, authored by Dr. Glen Brown, reframes digital currencies as nodes in a global kinetic energy matrix. The paper introduces the Kinetic Index Score (KIS), a four-dimensional Guidex Matrix, entropy regimes, and a complete integration with GATS, DAATS, and the Nine-Laws Framework to build structurally robust, energy-aware crypto portfolios.

-

Guidex Theory: Reframing Digital Currencies as a Global Kinetic Energy Matrix

- November 24, 2025

- Posted by: DrGlenBrown2

- Category: Digital Currencies / Macro-Theory / Crypto Valuation Models

Guidex Theory redefines Bitcoin and digital assets as nodes in a global kinetic energy matrix—transforming computational work and electrical power into digital reserves. Dr. Glen Brown introduces a new valuation and trading framework grounded in thermodynamics, entropy, and adaptive market regimes.

-

The Adaptive Quantum Doctrine of Breakevens & DAATS in GATS

- November 22, 2025

- Posted by: DrGlenBrown2

- Categories: Financial Engineering & Algorithmic Trading, Quantitative Risk Management

Discover how GATS integrates Fractional Breakevens, Post-BE Dissipation, and DAATS into a quantum-adaptive risk system that minimizes drawdown and maximizes trend survival.

-

Lecture 7: The Law of Drawdown in Time — Quantum Implications for Trade Longevity

- November 2, 2025

- Posted by: DrGlenBrown2

- Categories: GATS Lecture Series — Algorithmic Risk and Volatility Engineering, GATS Methodology

This lecture formalizes the GATS axiom that drawdown should cost time, not capital. We map equity drawdown to a temporal budget via ATR-regime geometry and codify how DS (Death-Stop), DAATS (Dynamic Adaptive ATR Trailing Stop), and the 18.75% Law synchronize to convert equity risk into structured time expenditure. We then extend this to portfolio heat, shock handling, and “Exit Only on Death” discipline, with quantitative tables and MT5/GATS implementation blocks.

-

Lecture 6: The Geometry of Time — Trade Lifecycles, Resonant Durations, and Temporal Compression within GATS

- November 2, 2025

- Posted by: DrGlenBrown2

- Categories: GATS Lecture Series — Algorithmic Risk and Volatility Engineering, GATS Methodology

This lecture develops the Temporal Geometry Model within the Global Algorithmic Trading Software (GATS). Each trade is treated as a temporal organism whose lifespan expands or contracts with volatility, multi-timeframe alignment, and the 18.75% adaptive law. We formalize Temporal Compression (TC), Resonant Duration (Tres), and Chrono-Risk Scaling, and provide MT5/GATS execution patterns that convert volatility into measurable time.

- 66 W Flagler Street, Suite 900-8535, Miami, FL 33130

- info@globalaccountancyinstitute.com

- +1 786-305-3315