-

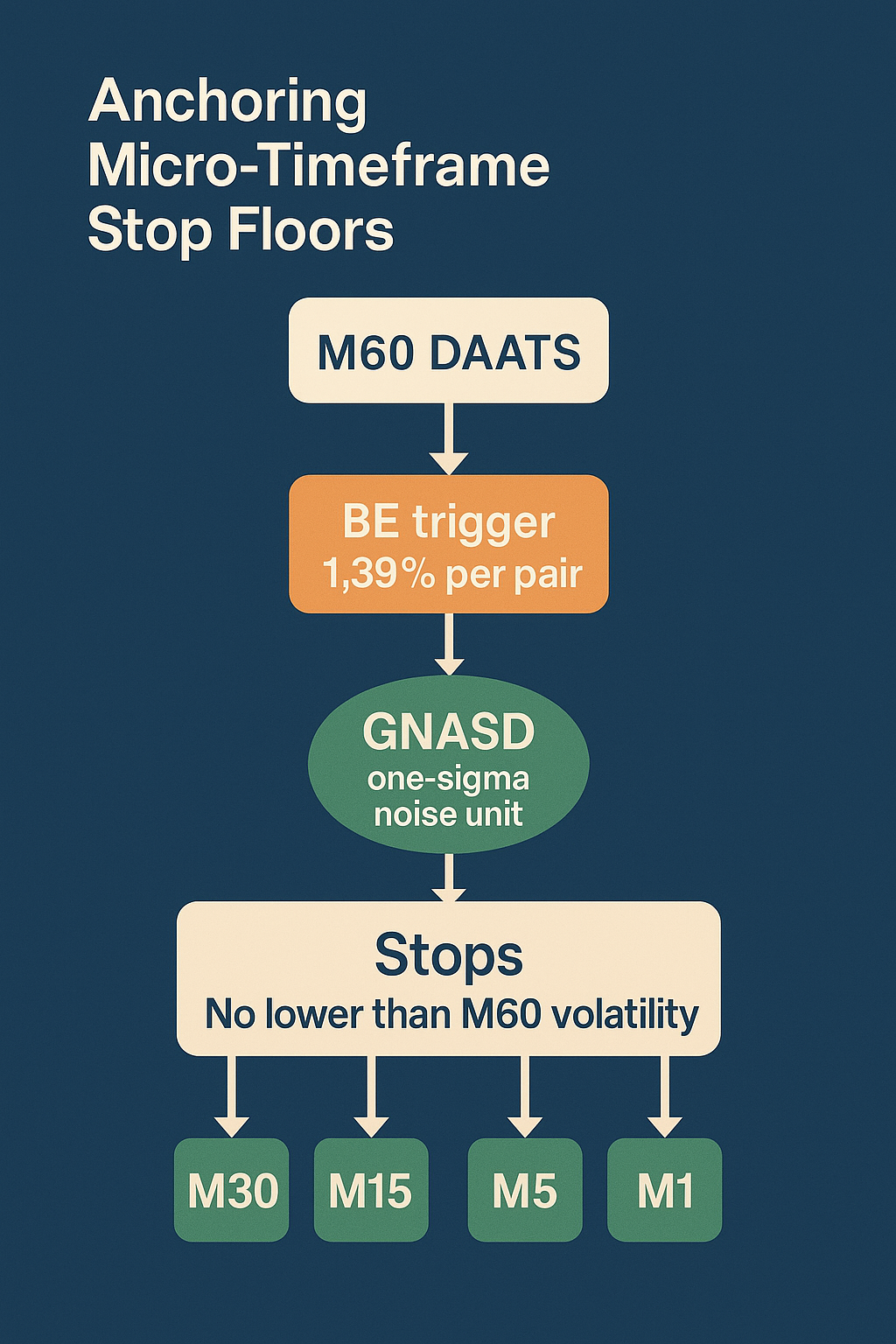

Micro‐Timeframe Stop Floors & Breakeven Logic Using M60 DAATS & GNASD

- May 31, 2025

- Posted by: DrGlenBrown2

- Category: GATS Methodology

No Comments

In this lecture, we demonstrate how GATS leverages M60 DAATS and the portfolio’s one‐sigma noise unit (GNASD) to establish robust stop‐loss floors, breakeven triggers, and trailing stops on M30, M15, M5, and M1. By anchoring micro‐timeframe stops to hourly volatility and applying a 1.39% breakeven rule per pair, traders can avoid routine hourly whipsaw while still capturing high‐probability moves under the Daily MACD bias and M60 EMA regime filters.

-

Law 7: GNASD—Managing Cross-Asset Noise Budgets

- May 25, 2025

- Posted by: DrGlenBrown2

- Category: Trading Methodology

Explore Law 7 of Dr. Glen Brown’s Seven Laws—GNASD for portfolio-level stops. Learn how to compute population σ, normalize by N, and apply global breakeven triggers with hybrid caps and cost floors.

-

Law 6: Tiered Risk Stages—Sizing to Match Your Buffer

- May 25, 2025

- Posted by: DrGlenBrown2

- Category: Trading Methodology

Learn Law 6 of Dr. Glen Brown’s Seven Laws: position sizing via (Equity×Risk %) ÷ DAATS, explore Stage 1/2/3 risk tiers, and see case studies on dollar-at-risk levels.

-

Law 3: DAATS—Your Full-Zone Initial Stop

- May 24, 2025

- Posted by: DrGlenBrown2

- Category: Trading Methodology

Discover Law 3 of Dr. Glen Brown’s Seven Laws: DAATS = √P×ATR(P). Learn the formula, Chebyshev’s worst-case guarantee, and see an example trade with DAATS plotted.

-

Beyond ATR: Introducing Dr. Glen Brown’s Seven Laws of Volatility Stop-Loss

- May 24, 2025

- Posted by: DrGlenBrown2

- Category: Trading Methodology

Discover why static ATR-based stops fail and explore Dr. Glen Brown’s Seven Laws of Volatility Stop-Loss—anchored by √time scaling, DAATS and GNASD—for a truly adaptive risk framework.

-

GASBET: The Global Adaptive Statistical Break-Even Trigger

- May 6, 2025

- Posted by: DrGlenBrown2

- Category: Algorithmic Trading / Risk Management

Explore the DAATS distance distribution, the GASBET

𝜅

𝜎

κσ trigger formula, visualization techniques, and trade-offs between manual and automated exits. -

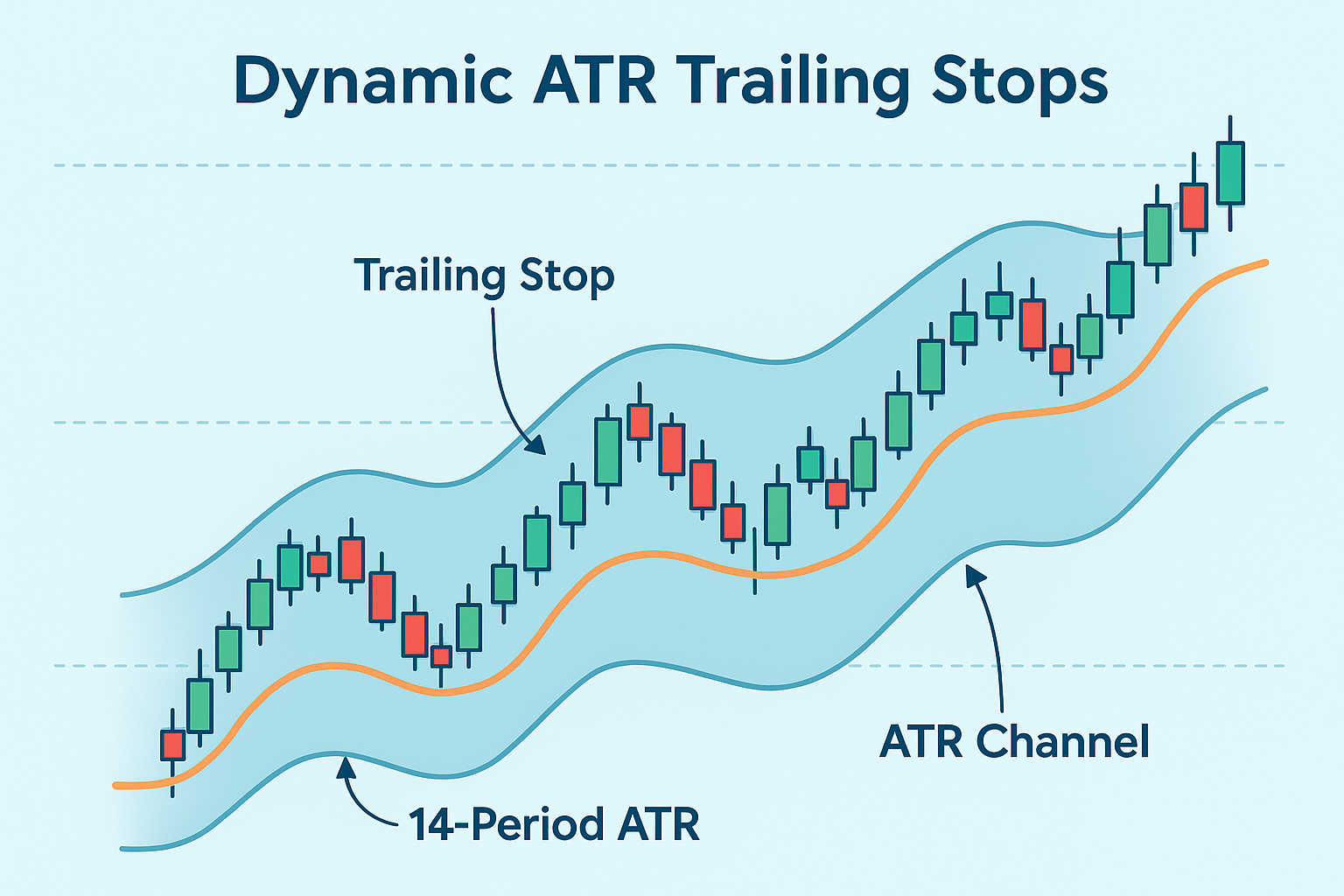

Dynamic Adaptive ATR Trailing Stops (DAATS): Volatility-Scaled Exits

- May 6, 2025

- Posted by: DrGlenBrown2

- Category: Risk Management / Algorithmic Trading

Learn how to deploy Dynamic Adaptive ATR Trailing Stops (DAATS) using ATR(89), square-root multipliers, and EMA zones to optimize trade exits.

-

GATS Unveiled: The Heartbeat of Global Financial Engineering

- April 25, 2025

- Posted by: DrGlenBrown2

- Category: Proprietary Trading / Algorithmic Trading

Discover how GFE’s home-grown GATS platform transforms market data into actionable strategies through its modular design, advanced risk tools, and nine timeframe-specific approaches.

-

The Closed-Loop Proprietary Model: Why GFE Keeps Innovation In-House

- April 25, 2025

- Posted by: DrGlenBrown2

- Category: Proprietary Trading

Discover how Global Financial Engineering’s 100% closed-loop proprietary model drives rapid innovation and protects intellectual property in algorithmic trading.

-

Global Adaptive Statistical Break-Even Trigger (GASBET) Model

- April 4, 2025

- Posted by: DrGlenBrown2

- Category: Financial Engineering

Explore the Global Adaptive Statistical Break-Even Trigger (GASBET) Model, which uses the statistical properties of DAATS values to set dynamic, market-responsive break-even points, ensuring superior risk management and profit capture.

- 66 W Flagler Street, Suite 900-8535, Miami, FL 33130

- info@globalaccountancyinstitute.com

- +1 786-305-3315